VNPY源码学习系列文章:

VNPY源码(一)CTP封装及K线合成

VNPY源码(二)API获取行情和script_trader

VNPY源码(三)主引擎MainEngine

VNPY源码(四)DataRecorder

VNPY源码(五)CtaEngine实盘引擎

VNPY源码(六)BacktesterEngine回测引擎

VNPY源码(七)限价单与停止单

VNPY源码(八)VNPY的数据流

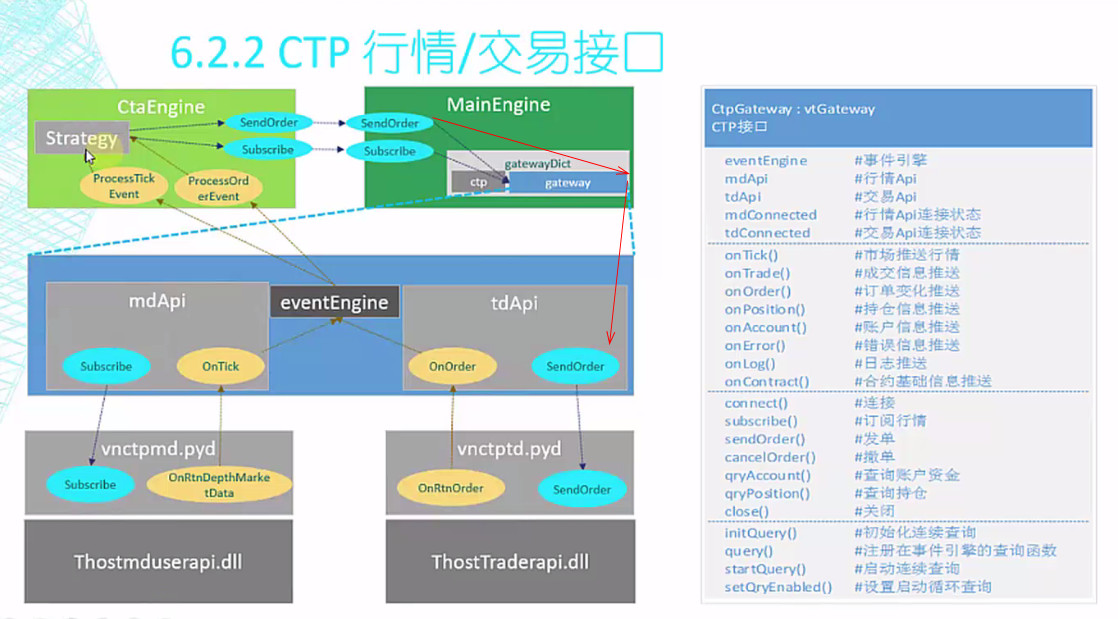

我觉得这张图是最清晰明了的:

策略通过CtaEngine向mdApi发送订阅行情的请求,返回tick交能eventEngine处理。

策略通过CtaEngine向tdApi发送订单相关的请求,返回order交能eventEngine处理。

至于eventEngine处理这些事件的原理,请看Vn.py学习记录十(事件驱动引擎)

尝试写一下自己理解的吧:

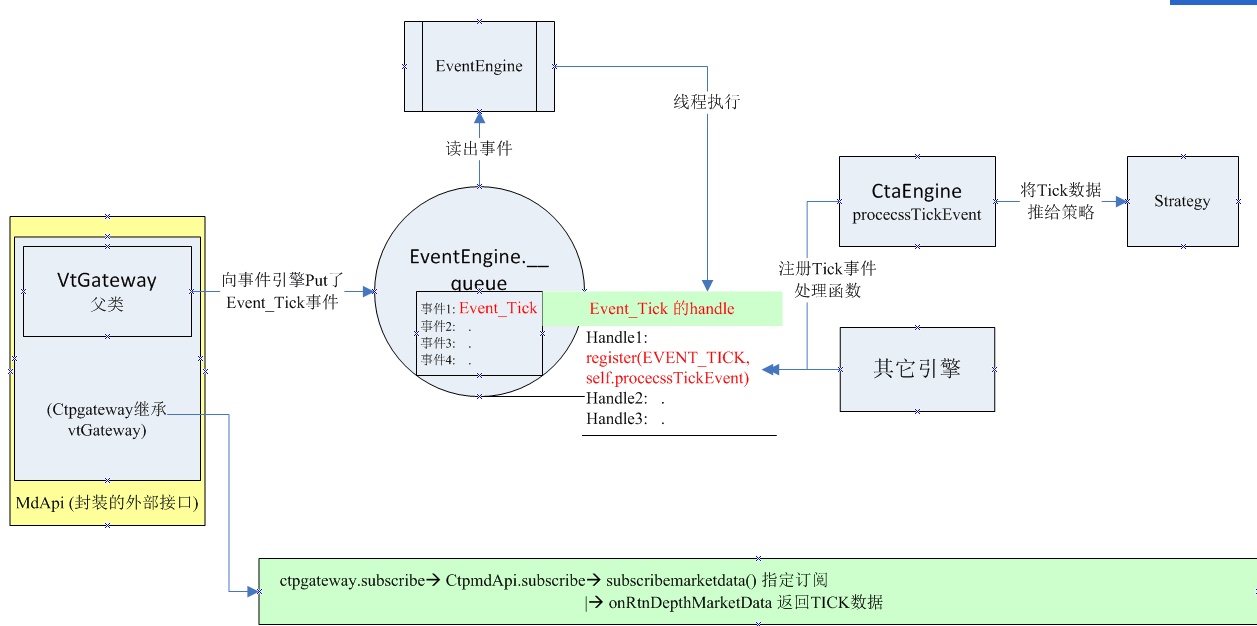

一、接收Tick数据到执行策略的流程:

1.ctaEngine对象向eventEngine中注册EVENT_TICK类型事件的处理函数句柄ctaEngine.processTickEvent

2.CTP的OnRtnDepthMarketData返回tick数据。

3.VNPY在OnRtnDepthMarketData中进行了处理,将data里的数据读取并转化成VtTickData对象,并调用ctpGateway.onTick函数,注册EVENT_TICK事件。

(1)OnRtnDepthMarketData

位于cnpy\gateway\ctp-tageway.py里面的class CtpMdApi(MdApi):

def onRtnDepthMarketData(self, data: dict):

"""

Callback of tick data update.

"""

symbol = data["InstrumentID"]

exchange = symbol_exchange_map.get(symbol, "")

if not exchange:

return

timestamp = f"{data['ActionDay']} {data['UpdateTime']}.{int(data['UpdateMillisec']/100)}"

tick = TickData(

symbol=symbol,

exchange=exchange,

datetime=datetime.strptime(timestamp, "%Y%m%d %H:%M:%S.%f"),

name=symbol_name_map[symbol],

volume=data["Volume"],

open_interest=data["OpenInterest"],

last_price=data["LastPrice"],

limit_up=data["UpperLimitPrice"],

limit_down=data["LowerLimitPrice"],

open_price=data["OpenPrice"],

high_price=data["HighestPrice"],

low_price=data["LowestPrice"],

pre_close=data["PreClosePrice"],

bid_price_1=data["BidPrice1"],

ask_price_1=data["AskPrice1"],

bid_volume_1=data["BidVolume1"],

ask_volume_1=data["AskVolume1"],

gateway_name=self.gateway_name

)

self.gateway.on_tick(tick)

(2)在ctpGateway里面没有onTick函数,它是在BaseGateway基类里面定义的。

class BaseGateway(ABC):

"""

Abstract gateway class for creating gateways connection

to different trading systems.

# How to implement a gateway:

---

## Basics

A gateway should satisfies:

* this class should be thread-safe:

* all methods should be thread-safe

* no mutable shared properties between objects.

* all methods should be non-blocked

* satisfies all requirements written in docstring for every method and callbacks.

* automatically reconnect if connection lost.

---

## methods must implements:

all @abstractmethod

---

## callbacks must response manually:

* on_tick

* on_trade

* on_order

* on_position

* on_account

* on_contract

All the XxxData passed to callback should be constant, which means that

the object should not be modified after passing to on_xxxx.

So if you use a cache to store reference of data, use copy.copy to create a new object

before passing that data into on_xxxx

"""

# Fields required in setting dict for connect function.

default_setting = {}

# Exchanges supported in the gateway.

exchanges = []

def __init__(self, event_engine: EventEngine, gateway_name: str):

""""""

self.event_engine = event_engine

self.gateway_name = gateway_name

def on_event(self, type: str, data: Any = None):

"""

General event push.

"""

event = Event(type, data)

self.event_engine.put(event)

def on_tick(self, tick: TickData):

"""

Tick event push.

Tick event of a specific vt_symbol is also pushed.

"""

self.on_event(EVENT_TICK, tick)

self.on_event(EVENT_TICK + tick.vt_symbol, tick)

4.ctpGateway.onTick函数将VtTickData对象包装成类型为EVENT_TICK的行情事件对象Event,并调用eventEngine.put函数,放入事件引擎的缓冲队列

5.事件引擎的工作线程,从缓冲队列中读取出最新的行情事件后,根据EVENT_TICK事件类型去查找缓存在内部字典中的处理函数列表,并将事件对象作为入参,遍历调用到列表中的处理函数ctaEngine.process_tick_event。

6.执行ctaEngine中的process_tick_event函数,通过Tick的代码vtSymbol,调用交易该代码合约的策略对象strategy.onTick函数,最终去运行策略中的逻辑

#vnpy/app/cta_strategy/engine.py

def process_tick_event(self, event: Event):

""""""

tick = event.data

strategies = self.symbol_strategy_map[tick.vt_symbol] #symbol_strategy_map是defaultdict,是vt_symbol: strategy list的形式。

if not strategies:

return

self.check_stop_order(tick)

for strategy in strategies:

if strategy.inited:

self.call_strategy_func(strategy, strategy.on_tick, tick)

二、主动订阅:

1.用户通过mainEngine.subscribe函数,发起订阅。

2.mainEngine.subscribe其实又是调用ctpGateway.subscribe函数

3.ctpGateway.subscribe中调用ctpMdApi.subscrbie函数

4.ctpMdApi.subscribe中调用C++封装的MdApi.subscribeMarketData函数,将订阅行情的请求最终通过底层C++ CTP API发出

三、流程描述

整个流程下来,不考虑stoporder,是ctaTemplate -> CtaEngine->mainEngine ->ctpgateway ->CtpTdApi, 传到C++封装的接口。返回的就是vtOrderID; 因为存在平昨,平今还有锁仓,反手等拆分情况,返回的可能是一组。

比如:

策略中的buy -> CTATemplate中的buy -> 其实是执行CTATemplate中的send_order -> 其实是调用self.cta_engine.send_order -> 根据限价单、停止单执行不同逻辑,如果是限价单,执行send_limit_order函数 —> 其实是调用send_server_order -> 调用main_engine.send_order -> 其实是调用gateway.send_order

最后,附一张官方推荐的图:

原载:蜗牛博客

网址:http://www.snailtoday.com

尊重版权,转载时务必以链接形式注明作者和原始出处及本声明。