一、结果

数据时间范围: 2025-06-06 09:31:00 至 2026-01-09 15:00:00

总分钟数: 35366

生成的基础因子列表:

['ret_1m', 'ret_5m', 'ret_15m', 'corr_vp', 'illiq', 'illiq_ma', 'up_vol', 'down_vol', 'imb', 'rv', 'rv_ratio', 'mom', 'overnight_ret', 'intraday_ret', 'reversal', 'upper_shadow', 'lower_shadow', 'pressure', 'vwap', 'vwap_dev', 'direction', 'buy_vol', 'sell_vol', 'net_vol', 'vol_ratio']

=== 开始遗传规划因子挖掘 ===

各因子缺失比例:

ret_1m 0.000028

ret_5m 0.000141

ret_15m 0.000424

corr_vp 0.000820

illiq_ma 0.000848

imb 0.000537

rv_ratio 0.004213

mom 0.000848

reversal 0.000679

pressure 0.000537

vwap_dev 0.000820

vol_ratio 0.000820

dtype: float64

实际用于遗传规划的因子列 (12个): ['ret_1m', 'ret_5m', 'ret_15m', 'corr_vp', 'illiq_ma', 'imb', 'rv_ratio', 'mom', 'reversal', 'pressure', 'vwap_dev', 'vol_ratio']

遗传规划可用数据行数: 35183(总行数: 35366)

=== 目标收益诊断 ===

count 35183.000000

mean 0.000032

std 0.003392

min -0.022635

25% -0.001720

50% 0.000000

75% 0.001729

max 0.027119

Name: future_ret_30, dtype: float64

标准差: 0.0033915940902883566

唯一值个数: 3480

因子 ret_1m 与目标收益的 Rank IC: -0.080238

因子 ret_5m 与目标收益的 Rank IC: -0.042970

因子 ret_15m 与目标收益的 Rank IC: -0.013608

[调试] 个体 #1 因子值统计:

均值: 0.211265, 标准差: 0.243985

最小值: 0.000000, 最大值: 0.968815

唯一值数量: 29917 (总样本: 35183)

表达式: maximum(safe_sqrt(add(imb, ret_15m)), absolute(multiply(ret_5m, imb)))

[调试] 个体 #2 因子值统计:

均值: 0.357712, 标准差: 0.191625

最小值: -0.424701, 最大值: 0.925192

唯一值数量: 32303 (总样本: 35183)

表达式: maximum(reversal, imb)

[调试] 个体 #3 因子值统计:

均值: -482.225127, 标准差: 3795.481609

最小值: -31941.113993, 最大值: 30077.296492

唯一值数量: 35183 (总样本: 35183)

表达式: add(safe_div(safe_div(imb, mom), safe_sqrt(mom)), absolute(subtract(ret_15m, rv_ratio)))

gen nevals avg max

0 100 0 0

1 76 0 0

2 72 0 0

3 66 0 0

4 65 0 0

5 71 0 0

6 73 0 0

7 76 0 0

8 71 0 0

9 78 0 0

10 74 0 0

11 66 0 0

12 65 0 0

13 70 0 0

14 68 0 0

15 76 0 0

16 69 0 0

17 71 0 0

18 75 0 0

19 76 0 0

20 68 0 0

最佳因子表达式: maximum(safe_sqrt(add(imb, ret_15m)), absolute(multiply(ret_5m, imb)))

遗传规划因子已保存至 'gp_factor' 列。

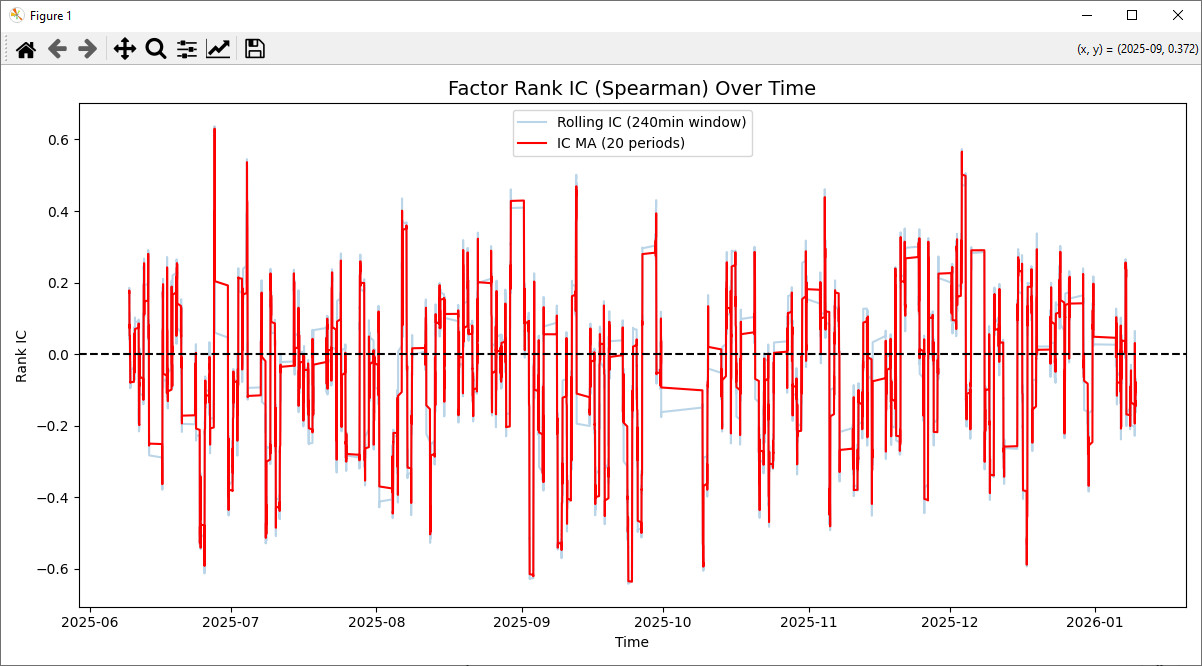

=== 单资产因子 IC 分析 ===

有效分析行数: 35336

Rank IC 均值: -0.045576

Rank IC 标准差: 0.203547

IR (Information Ratio): -0.2239

IC 正比例: 42.87%

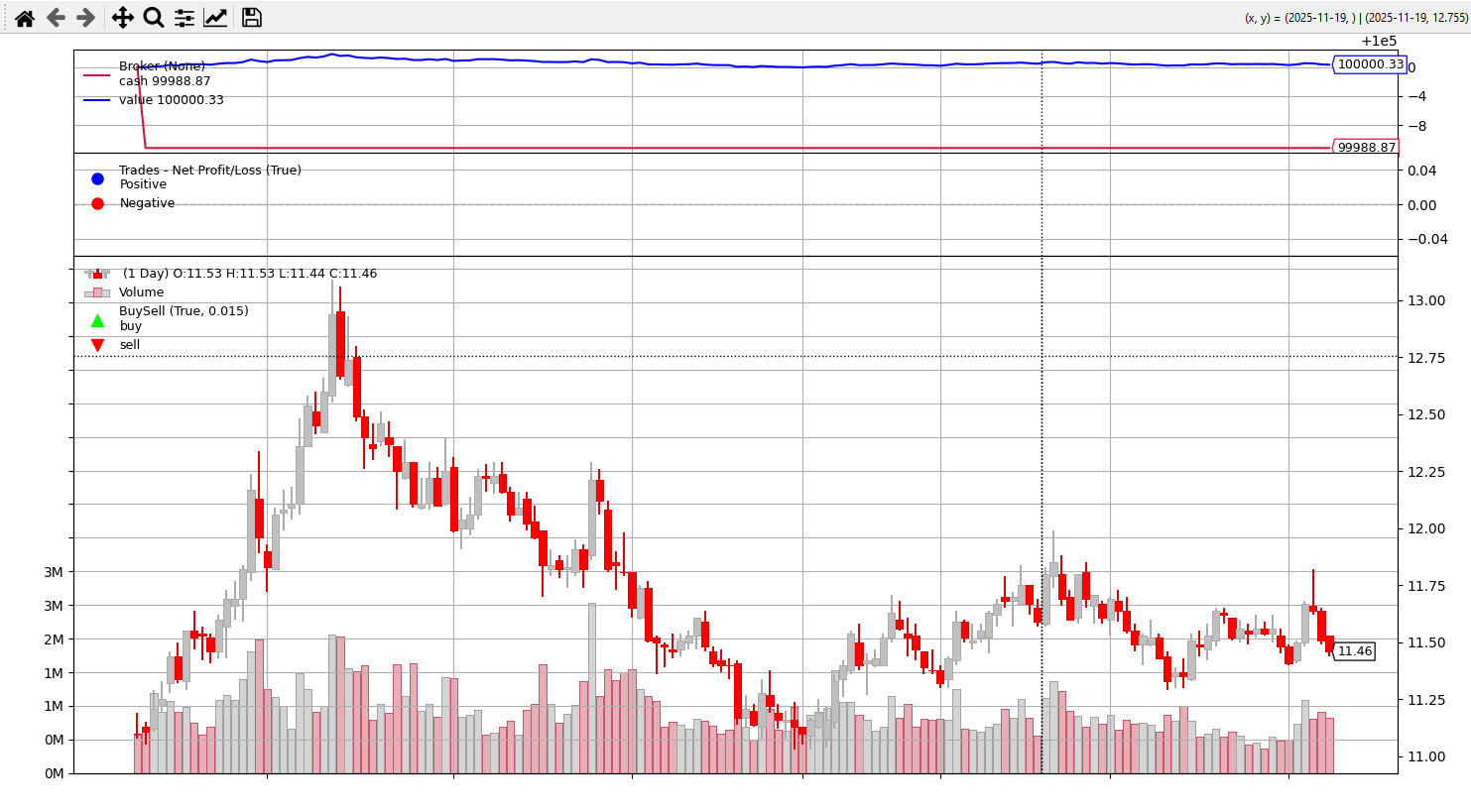

=== Backtrader策略回测 ===

初始资金: 100000.00

最终资金: 100000.33

年化收益率: 0.00%

夏普比率: -8822.30

最大回撤: 0.00%

PS I:\量化交易\yinzi>

二、代码

# ==================== 0. 环境准备 ====================

import pandas as pd

import numpy as np

import random

from datetime import datetime, time

import warnings

warnings.filterwarnings('ignore')

# 遗传规划库

from deap import base, creator, tools, gp, algorithms

# 因子分析库

import alphalens as al

# 回测库

import backtrader as bt

import backtrader.analyzers as btanalyzers

# ==================== 1. 数据加载与预处理 ====================

# 假设数据已保存为 'data.csv',格式与你给出的样例一致

df_raw = pd.read_csv('data.csv', encoding='gbk')

# 合并日期和时间列,生成精确到分钟的datetime索引

df_raw['datetime'] = pd.to_datetime(df_raw['日期'].astype(str) + ' ' + df_raw['时间'])

df_raw.drop(['日期', '时间'], axis=1, inplace=True)

df_raw.set_index('datetime', inplace=True)

df_raw.sort_index(inplace=True)

# 提取股票代码(假设只有一只股票,但保留结构以支持多只)

stock_code = df_raw['股票代码'].iloc[0]

# 仅保留需要的OHLCV列

df = df_raw[['open', 'high', 'low', 'close', 'volume', '成交额']].copy()

df.rename(columns={'成交额': 'amount'}, inplace=True)

# 过滤集合竞价时段 (9:15-9:25) —— 根据样例,数据从9:31开始,无需过滤,但保留逻辑

def is_trading_time(ts):

t = ts.time()

morning = (time(9,30) <= t <= time(11,30))

afternoon = (time(13,0) <= t <= time(15,0))

return morning or afternoon

df = df[df.index.map(is_trading_time)]

print(f"数据时间范围: {df.index[0]} 至 {df.index[-1]}")

print(f"总分钟数: {len(df)}")

# ==================== 2. 基础因子计算引擎(1分钟专用) ====================

class OneMinFactorGenerator:

def __init__(self, df_min):

self.df = df_min.copy()

self.df.sort_index(inplace=True)

def factor_returns(self):

self.df['ret_1m'] = self.df['close'].pct_change()

self.df['ret_5m'] = self.df['close'].pct_change(5)

self.df['ret_15m'] = self.df['close'].pct_change(15)

return self.df[['ret_1m', 'ret_5m', 'ret_15m']]

def factor_volume_price_corr(self, window=30):

self.df['corr_vp'] = self.df['volume'].rolling(window).corr(self.df['close'])

return self.df[['corr_vp']]

def factor_illiquidity(self, window=30):

self.df['illiq'] = np.abs(self.df['ret_1m']) / (self.df['amount'] / 1e6)

self.df['illiq_ma'] = self.df['illiq'].rolling(window).mean()

return self.df[['illiq_ma']]

def factor_order_imbalance(self, window=20):

self.df['up_vol'] = np.where(self.df['close'] > self.df['open'], self.df['volume'], 0)

self.df['down_vol'] = np.where(self.df['close'] < self.df['open'], self.df['volume'], 0)

self.df['imb'] = (self.df['up_vol'].rolling(window).sum() -

self.df['down_vol'].rolling(window).sum()) / \

(self.df['volume'].rolling(window).sum() + 1e-9)

return self.df[['imb']]

def factor_high_freq_volatility(self, window=30):

self.df['rv'] = np.sqrt((self.df['ret_1m']**2).rolling(window).sum() * 240)

self.df['rv_ratio'] = self.df['rv'] / self.df['rv'].rolling(120).mean()

return self.df[['rv_ratio']]

def factor_intraday_momentum(self, short=10, long=30):

self.df['mom'] = self.df['close'].pct_change(short) - self.df['close'].pct_change(long)

return self.df[['mom']]

def factor_intraday_reversal(self, window=20):

self.df['overnight_ret'] = self.df['open'] / self.df['close'].shift(1) - 1

self.df['intraday_ret'] = self.df['close'] / self.df['open'] - 1

self.df['reversal'] = -self.df['overnight_ret'].rolling(window).corr(self.df['intraday_ret'])

return self.df[['reversal']]

def factor_order_book_pressure(self, window=20):

self.df['upper_shadow'] = (self.df['high'] - np.maximum(self.df['open'], self.df['close'])) / self.df['close']

self.df['lower_shadow'] = (np.minimum(self.df['open'], self.df['close']) - self.df['low']) / self.df['close']

self.df['pressure'] = (self.df['upper_shadow'].rolling(window).mean() -

self.df['lower_shadow'].rolling(window).mean())

return self.df[['pressure']]

def factor_vwap_deviation(self, window=30):

self.df['vwap'] = (self.df['amount'] / self.df['volume']).rolling(window).mean()

self.df['vwap_dev'] = self.df['close'] / self.df['vwap'] - 1

return self.df[['vwap_dev']]

def factor_tick_rule_volume(self, window=30):

self.df['direction'] = np.sign(self.df['close'].diff())

self.df['buy_vol'] = np.where(self.df['direction'] > 0, self.df['volume'], 0)

self.df['sell_vol'] = np.where(self.df['direction'] < 0, self.df['volume'], 0)

self.df['net_vol'] = (self.df['buy_vol'].rolling(window).sum() -

self.df['sell_vol'].rolling(window).sum())

self.df['vol_ratio'] = self.df['net_vol'] / (self.df['volume'].rolling(window).sum() + 1e-9)

return self.df[['vol_ratio']]

def generate_all_factors(self):

self.factor_returns()

self.factor_volume_price_corr()

self.factor_illiquidity()

self.factor_order_imbalance()

self.factor_high_freq_volatility()

self.factor_intraday_momentum()

self.factor_intraday_reversal()

self.factor_order_book_pressure()

self.factor_vwap_deviation()

self.factor_tick_rule_volume()

return self.df

# 生成基础因子

gen = OneMinFactorGenerator(df)

factor_df = gen.generate_all_factors()

print("\n生成的基础因子列表:")

print(])

# ==================== 3. 因子预处理与涨跌停屏蔽 ====================

def handle_limit_up_down(df, limit_threshold=0.095):

df['limit_up'] = (df['close'].pct_change() > limit_threshold)

df['limit_down'] = (df['close'].pct_change() < -limit_threshold)

# 触及涨跌停后因子值置NaN

factor_cols = ]

for col in factor_cols:

df.loc[df['limit_up'] | df['limit_down'], col] = np.nan

return df

factor_df = handle_limit_up_down(factor_df)

# ==================== 4. 遗传规划因子挖掘(DEAP) ====================

print("\n=== 开始遗传规划因子挖掘 ===")

# ---------- 4.1 筛选有效因子列 ----------

factor_columns = ['ret_1m', 'ret_5m', 'ret_15m', 'corr_vp', 'illiq_ma',

'imb', 'rv_ratio', 'mom', 'reversal', 'pressure', 'vwap_dev', 'vol_ratio']

missing_ratio = factor_df[factor_columns].isnull().mean()

print("各因子缺失比例:")

print(missing_ratio)

valid_factor_cols = missing_ratio[missing_ratio <= 0.8].index.tolist()

print(f"\n实际用于遗传规划的因子列 ({len(valid_factor_cols)}个): {valid_factor_cols}")

# ---------- 4.2 构建遗传规划数据集 ----------

factor_df['future_ret_30'] = factor_df['close'].pct_change(30).shift(-30)

gp_data = factor_df[valid_factor_cols + ['future_ret_30']].dropna()

print(f"遗传规划可用数据行数: {len(gp_data)}(总行数: {len(factor_df)})")

# 诊断目标收益质量

print("\n=== 目标收益诊断 ===")

print(gp_data['future_ret_30'].describe())

print("标准差:", gp_data['future_ret_30'].std())

print("唯一值个数:", gp_data['future_ret_30'].nunique())

for col in valid_factor_cols[:3]:

ic = gp_data[col].corr(gp_data['future_ret_30'], method='spearman')

print(f"因子 {col} 与目标收益的 Rank IC: {ic:.6f}")

# ---------- 4.3 定义遗传规划类型 ----------

creator.create("FitnessMax", base.Fitness, weights=(1.0,))

creator.create("Individual", gp.PrimitiveTree, fitness=creator.FitnessMax)

# ---------- 4.4 构建原语集 ----------

pset = gp.PrimitiveSet("MAIN", arity=len(valid_factor_cols))

def safe_div(x, y):

return np.divide(x, y, out=np.zeros_like(x), where=(np.abs(y) > 1e-9))

def safe_log(x):

return np.log(np.maximum(np.abs(x), 1e-9))

def safe_sqrt(x):

return np.sqrt(np.maximum(x, 0))

pset.addPrimitive(np.add, 2)

pset.addPrimitive(np.subtract, 2)

pset.addPrimitive(np.multiply, 2)

pset.addPrimitive(safe_div, 2)

pset.addPrimitive(np.negative, 1)

pset.addPrimitive(np.abs, 1)

pset.addPrimitive(safe_log, 1)

pset.addPrimitive(safe_sqrt, 1)

pset.addPrimitive(np.maximum, 2)

pset.addPrimitive(np.minimum, 2)

for i, name in enumerate(valid_factor_cols):

pset.renameArguments(**{f'ARG{i}': name})

# ---------- 4.5 注册工具 ----------

toolbox = base.Toolbox()

toolbox.register("expr", gp.genHalfAndHalf, pset=pset, min_=1, max_=3)

toolbox.register("individual", tools.initIterate, creator.Individual, toolbox.expr)

toolbox.register("population", tools.initRepeat, list, toolbox.individual)

toolbox.register("compile", gp.compile, pset=pset)

# ---------- 4.6 评估函数(含调试打印 + 注册) ----------

_print_counter = 0 # 全局计数器,避免打印泛滥

def eval_individual(individual):

global _print_counter

func = toolbox.compile(expr=individual)

args = {name: gp_data[name].values for name in valid_factor_cols}

factor_values = func(**args)

factor_values = np.asarray(factor_values).ravel()

# 处理非法值

factor_values = np.nan_to_num(factor_values, nan=0.0, posinf=0.0, neginf=0.0)

# 打印前3个个体的统计信息

_print_counter += 1

if _print_counter <= 3:

print(f"\n[调试] 个体 #{_print_counter} 因子值统计:")

print(f" 均值: {factor_values.mean():.6f}, 标准差: {factor_values.std():.6f}")

print(f" 最小值: {factor_values.min():.6f}, 最大值: {factor_values.max():.6f}")

print(f" 唯一值数量: {len(np.unique(factor_values))} (总样本: {len(factor_values)})")

print(f" 表达式: {individual}")

# 如果标准差极小(几乎为常数),直接返回0

if np.std(factor_values) < 1e-8:

return (0.0,)

ic = pd.Series(factor_values).corr(gp_data['future_ret_30'], method='spearman')

if np.isnan(ic):

return (0.0,)

return (abs(ic),)

# ⚠️ 这一行绝对不能少!

toolbox.register("evaluate", eval_individual)

toolbox.register("select", tools.selTournament, tournsize=3)

toolbox.register("mate", gp.cxOnePoint)

toolbox.register("expr_mut", gp.genFull, min_=0, max_=2)

toolbox.register("mutate", gp.mutUniform, expr=toolbox.expr_mut, pset=pset)

# ---------- 4.7 运行遗传算法 ----------

pop = toolbox.population(n=100) # 增大种群

hof = tools.HallOfFame(1)

stats = tools.Statistics(lambda ind: ind.fitness.values)

stats.register("avg", np.mean)

stats.register("max", np.max)

pop, log = algorithms.eaSimple(pop, toolbox, cxpb=0.5, mutpb=0.4, ngen=20, # 更多代、更高变异

stats=stats, halloffame=hof, verbose=True)

best_ind = hof[0]

print("\n最佳因子表达式:", best_ind)

# ---------- 4.8 计算全数据因子值 ----------

func = toolbox.compile(expr=best_ind)

args_full = {name: factor_df[name].fillna(0).values for name in valid_factor_cols}

factor_values_full = np.asarray(func(**args_full)).ravel()

factor_df['gp_factor'] = factor_values_full

print("遗传规划因子已保存至 'gp_factor' 列。")

# ==================== 5. 单资产因子 IC 分析(无 Alphalens 分箱) ====================

print("\n=== 单资产因子 IC 分析 ===")

# ---------- 5.1 准备分析数据 ----------

# 使用原始交易分钟数据(不扩展连续索引)

analysis_data = factor_df[['close', 'gp_factor']].copy()

# 计算未来30分钟收益率

analysis_data['forward_ret_30m'] = analysis_data['close'].pct_change(30).shift(-30)

# 删除 NaN

analysis_data.dropna(inplace=True)

print(f"有效分析行数: {len(analysis_data)}")

# ---------- 5.2 滚动 IC 计算 ----------

# 每 240 分钟(约1天)滚动窗口,计算 Spearman Rank IC

window_size = 240 # 约1个交易日

rolling_ic = []

for i in range(window_size, len(analysis_data)):

window = analysis_data.iloc[i-window_size:i]

ic = window['gp_factor'].corr(window['forward_ret_30m'], method='spearman')

rolling_ic.append({

'time': analysis_data.index[i],

'ic': ic

})

rolling_ic_df = pd.DataFrame(rolling_ic).set_index('time')

rolling_ic_df['ic_ma'] = rolling_ic_df['ic'].rolling(20).mean() # 平滑

# ---------- 5.3 打印关键统计 ----------

mean_ic = rolling_ic_df['ic'].mean()

std_ic = rolling_ic_df['ic'].std()

ir = mean_ic / std_ic if std_ic != 0 else 0

print(f"Rank IC 均值: {mean_ic:.6f}")

print(f"Rank IC 标准差: {std_ic:.6f}")

print(f"IR (Information Ratio): {ir:.4f}")

print(f"IC 正比例: {(rolling_ic_df['ic'] > 0).mean() * 100:.2f}%")

# ---------- 5.4 绘制 IC 时间序列 ----------

import matplotlib.pyplot as plt

plt.figure(figsize=(12, 6))

plt.plot(rolling_ic_df.index, rolling_ic_df['ic'], alpha=0.3, label='Rolling IC (240min window)')

plt.plot(rolling_ic_df.index, rolling_ic_df['ic_ma'], color='red', label='IC MA (20 periods)')

plt.axhline(y=0, color='black', linestyle='--')

plt.title('Factor Rank IC (Spearman) Over Time', fontsize=14)

plt.xlabel('Time')

plt.ylabel('Rank IC')

plt.legend()

plt.tight_layout()

plt.show()

# ==================== 6. Backtrader策略回测 ====================

print("\n=== Backtrader策略回测 ===")

# 准备回测数据:日线数据(策略为每日开盘计算因子信号)

# 将1分钟数据降采样为日线(开高低收+成交量)

daily_df = factor_df.resample('1D').agg({

'open': 'first',

'high': 'max',

'low': 'min',

'close': 'last',

'volume': 'sum',

'gp_factor': 'last' # 使用每日最后一分钟的因子值

}).dropna()

class GPFactorStrategy(bt.Strategy):

params = (

('threshold', 0.5), # 因子信号阈值

)

def __init__(self):

self.factor = self.datas[0].gp_factor

self.order = None

def next(self):

if self.order:

return

# 每日开盘判断

if self.factor[0] > self.params.threshold:

# 买入信号

self.order = self.buy()

elif self.factor[0] < -self.params.threshold:

# 卖出信号(若允许做空,此处为sell;A股做空受限,可空仓)

self.order = self.sell()

else:

# 空仓

if self.position:

self.order = self.close()

# 构造Backtrader数据源

class PandasData(bt.feeds.PandasData):

lines = ('gp_factor',)

params = (

('datetime', None),

('open', 'open'),

('high', 'high'),

('low', 'low'),

('close', 'close'),

('volume', 'volume'),

('gp_factor', 'gp_factor'),

)

cerebro = bt.Cerebro()

data = PandasData(dataname=daily_df)

cerebro.adddata(data)

# 设置初始资金

cerebro.broker.setcash(100000.0)

cerebro.broker.setcommission(commission=0.0003) # 万三佣金

# 添加策略

cerebro.addstrategy(GPFactorStrategy, threshold=0.3)

# 添加分析器

cerebro.addanalyzer(btanalyzers.SharpeRatio, _name='sharpe')

cerebro.addanalyzer(btanalyzers.Returns, _name='returns')

cerebro.addanalyzer(btanalyzers.DrawDown, _name='drawdown')

# 运行回测

print('初始资金: %.2f' % cerebro.broker.getvalue())

results = cerebro.run()

print('最终资金: %.2f' % cerebro.broker.getvalue())

# 输出分析结果

strat = results[0]

print('年化收益率: %.2f%%' % (strat.analyzers.returns.get_analysis()['rnorm100']))

print('夏普比率: %.2f' % strat.analyzers.sharpe.get_analysis()['sharperatio'])

print('最大回撤: %.2f%%' % strat.analyzers.drawdown.get_analysis()['max']['drawdown'])

# 绘制回测曲线

cerebro.plot(style='candlestick')